- 🔥 🌶 HOT SAUCE 🌶 🔥

- Posts

- 250k check size is not ideal

Small TAM on this post, but I think there are alot of emerging managers raising fund 1s and planning on writing $250K checks so I wanted to share my learnings. We have 50 portfolio companies in so I think its a decent sample size to draw conclusions from.

First of all, portfolio construction is so weird. Everyone has a slightly different POV (which is good! - how else can you promise alpha if everyone has the same strategy). Ryan Hoover and Vedika Jain of Weekend Fund pulled together a great blog post which shows the difference in opinions:

As an emerging manager, $250K check size is a common strategy and could put you in no-mans land. Open to debate on this! Would love to be challenged on my assumptions. I’m still early in my career and learning.

Ok so why is $250K risky?

First it depends on type of investor you are/plan to be →

For high-conviction first-check investors:

game of taste - you must have imagination

You can give a founder their first 250K, but you may leave them stranded right as they are getting momentum. Many emerging managers don’t have high “signal” and other people don’t pile in to co-invest the way they do if it is a brand name VC. This has kept me up many nights. Amazing companies with all the right traction, but not enough runway because I chose to take them off-market and be the first check with only a $200k investment. (It is painful but in Spice’s case it worked out in the end. Good businesses get funded or find a way to get profitable quick)

Pros:

| Cons:

|

For follow-on investors:

game of access - this is a sales job

If you have no conviction yourself, your job is to convince founders/ lead investors to let you onto the cap table. You have to rely on other investors to set the terms. You will have less fear of the startup running out of money, but your returns will match those of the lead investors (arguably worse if you don’t get enough ownership). If you want to raise a larger fund down the line - how will you defend that you are a better allocator of big checks than the leads you co-invest with?

Pros:

| Cons:

|

Here are some ideas for fund portfolio construction:

Simplifying by using Fred Wilson’s sample model on his blog post (seed rounds at 100M valuations)

I like diversification. Especially when you are first building a brand in market (and learning what it’s like to be a GP) According to Angellist - seed stage companies have a 1 in 40 shot of picking a unicorn

To me, these are your two realistic options if you are an emerging manager wanting to do pre-seed. Both have fantastic return outcomes.

Be a great value-add co-investor - write maximum $100K checks

Be high conviction and co-lead/lead a seed round with at minimum $500K checks

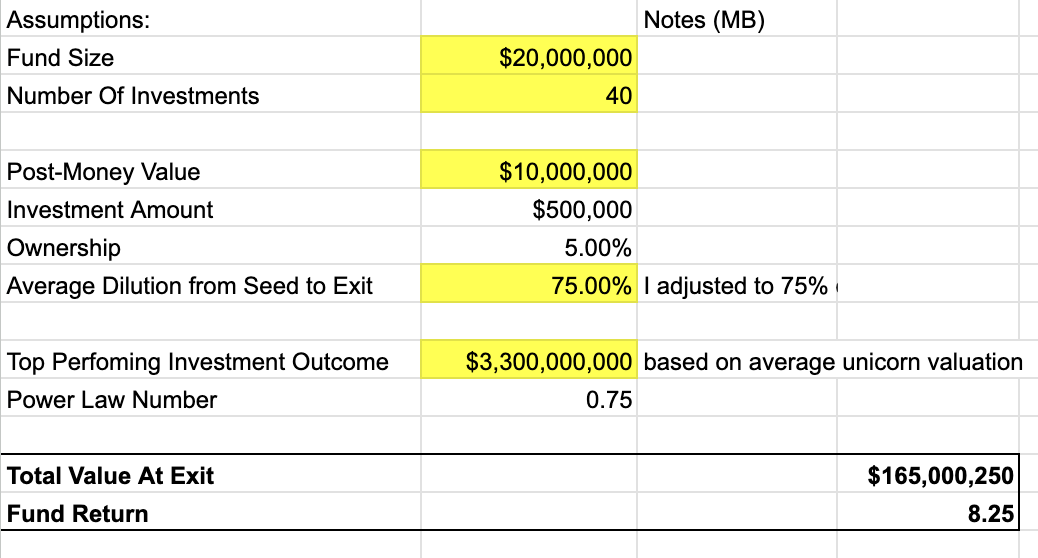

Option 1: 5M fund, ~100K checks

Option 2: 20M FUND, ~$500K CHECKS

Common pushbacks to my recommendation

Why not do less investments?

Why not play the venture odds if you are on a Fund 1? Early-stage is risky enough.

Exit valuation prediction should be higher ($10B) so entry shouldn’t matter as much

We saw last year that it is not always the case. There are also amazing $1B companies that are revolutionizing industries that you would have to walk away from.

Why not save more for reserves?

I believe there’s often false positive signaling at Series A. Many companies raise their A as soon as they cross the 1-5M ARR mark. Harder to sustain the 30% Month-over-Month growth in the $5M ARR range. Additionally, sometimes the valuation step up from Seed to Series A is so large you can’t do your full pro-rata anyways. I believe in earning ownership with the first check.

Can’t entry valuation be sub-$10M?

Yes - but only very very few VCs have the conviction to be first-check ^see post above. I have noticed most emerging managers wan’t other signal before cutting a check and that means price goes UP!

Caveats:

this only applies to a non-zirp market! In Zirp era, companies take on more capital in bull markets so you need to adjust your fund size “for inflation”.

I’m assuming a standard cap table setup at the pre-seed for a Tier-1 company: Usually 1 Lead aiming for 10%-20% of the company, and some operator angels/small funds for up to 5% of the company. Assuming a 10M post-money valuation, that leaves $500K for everyone besides the lead investor.

I’m sorry to the founders who I didn’t have enough money for. You know who you are and despite less funding in the early days you have absolutely smashed 🌶️.